Buying a House in New Zealand #1

First, a disclaimer: this article is not a home-buying guide. It won’t cover everything, it’s just my personal experience — not universally applicable, and I can’t even guarantee its accuracy. If you buy a house based on this article and step on a landmine, you’re on your own. Also, I’m an ordinary person. I don’t want to invest, I don’t want to speculate in property. I just want a home for myself. I hate the groups and individuals driving up housing prices. I, too, wish for millions of houses to shelter the world’s cold and weary. Unfortunately, even in sparsely populated New Zealand, that dream remains out of reach.

Background

After deciding in 2016 to move to New Zealand, we sold our Shanghai apartment and transferred the money to New Zealand before the end of 2016. So I can’t answer questions about current foreign exchange controls, nor can I tell you how to move money abroad via Bitcoin or underground banks — I didn’t have to deal with that.

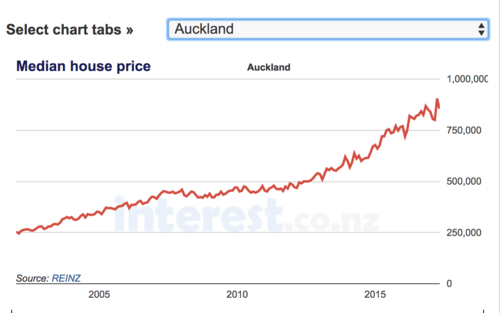

In most parts of New Zealand, any average apartment in Beijing, Shanghai, or Guangzhou could buy you a large farm with a herd of alpacas — no exaggeration. But Auckland, where we live, is the country’s largest city, home to a third of the population. Housing is still tight there. During our immigrant orientation, the teacher showed us a chart of Auckland’s median house prices over the past 20 years. If you know anything about machine learning or AI, no matter which regression model you use, the line is basically straight up. No major fluctuations. In 20 years, prices have steadily quadrupled. Of course, that’s nothing compared to China’s quadrupling in 4 years. But in the most sparsely populated country on earth, it’s still alarming. However, since China tightened foreign exchange controls last year, many people can’t get their money out, directly causing Auckland’s property market to slump — and it remains that way today.

House prices in NZ are basically two components: building + land. Generally, land is more expensive than the building. Of course, you can buy vacant land and hire someone to design and build, but given local efficiency, you probably won’t move in for 3–5 years. Unlike China, there are very few new homes here. Most are decades old, third- or fourth-hand. The house I bought is from the 1980s. So I’ll only talk about buying existing homes.

NZ homes are also linked to school zones — school district properties exist here too. But this is a classic case of “rental equals ownership”: as long as you rent a house near the school, even sharing, your child can attend. You just need any bill with your name on it. Nobody checks if it’s fake or if multiple people are using the same address. Of course, school zones and education are a whole other topic — I’ll write about it separately if I get the chance.

This article won’t analyse future price trends — just my buying experience, comparisons with my experience buying in Shanghai, and some personal observations.

Pre-approval and Loans

Like in China, most people buy houses with loans. According to Wiki, New Zealand’s average annual income is about NZ$55,000, while Auckland’s median house price is NZ$900,000. The down payment is only 10%, so a couple could save up for a down payment in a year or two. In theory, buying should be manageable. But since Kiwis tend to live paycheck to paycheck without much savings, someone who can put down 15% is considered a “土豪” (tycoon). New Zealand doesn’t have a housing provident fund — only KiwiSaver, which isn’t mandatory.

Unless you’re paying cash, everyone needs pre-approval from a bank. Pre-approval means the bank assesses your income and tells you the maximum they’ll lend. From my experience, pre-approval is very loose. Not long after I started working, I wandered into a bank during lunch. I asked about pre-approval. The teller said to come back tomorrow since the person in charge wasn’t in. I went back the next day, chatted with the bank manager for a few minutes, and walked out with NZ$500,000 pre-approval on the spot.

Compared to China, I think NZ banks’ risk control is extremely rough. They don’t even have loan-to-income ratios. The media had been hinting about introducing one, but they feared it would make it even harder for low-income people to buy homes, so they dropped it. As long as the bank thinks you’re reliable enough to repay, it’s fine. I suspect that with a high enough down payment, even without stable income, you could get a loan. If you default, the bank just auctions the house.

Compared to going directly to banks, New Zealand also has mortgage brokers — something China doesn’t have. They negotiate with various banks to get you the best deal. Since different banks in NZ offer very different services — unlike China, where the central bank treats everyone like its children — brokers serve a real purpose. I contacted the bank directly, so I don’t know much about brokers.

Because the central bank doesn’t micromanage, NZ mortgages come in all shapes and sizes. There are fixed rates, floating rates, and revolving credit. The Chinese-style mortgage basically corresponds to NZ’s one-year fixed rate, adjusted annually. Let me focus on the most peculiar one: revolving credit. Essentially, it’s like a credit card with an enormous limit. You use it to buy a house and only need to make minimum payments each month, just like a credit card. You can pay down the mortgage any time, and the next day, the repaid amount stops accruing interest. If you win the lottery today, you can pay off the mortgage tomorrow. Conversely, if you’re short on cash, you can redraw the repaid amount. My mortgage includes NZ$100,000 in revolving credit. Every day, I open the mobile app and see the interest grow by about a dozen dollars — like a reverse Yu’e Bao. A constant reminder of my mortgage slave status.

After I finalised the mortgage, the bank gave me a platinum credit card. I was surprised — is a platinum card here that worthless? In China, I used a credit card for ten years before being upgraded to platinum. The bank staff said, “Well, we’ve already given you NZ$100,000 in revolving credit, so an extra card is nothing.”

House Hunting

Once you have pre-approval, you can start house hunting. Like in China, buying a house mainly involves agents. You can count NZ’s nationwide real estate brands on one hand — nothing like China’s countless independent agencies everywhere. The process is similar to China: you look at houses currently on the market through Open Homes. Houses are open for viewing briefly — usually just two hours on Saturday or Sunday. After about a month of Open Homes, auctions begin.

Thanks to the formidable purchasing power of Chinese buyers in recent years, almost every Open Home now has a Chinese agent paired with a local one. The Chinese agent should speak Mandarin, Cantonese, and English — preferably Mandarin, Cantonese, English, and Shanghainese. I met one incredibly versatile agent. When Taiwanese viewers came, her voice turned all sweet like Lin Chi-ling: “This house is sooo comfy, you know?” Then when they left and Northeasterners arrived, her accent switched to something like Ai Fukuhara: “This house is wicked good, no drama.” To this day, I don’t know if she’s Marilyn from Taipei or Ma Lili from Dongbei.

Over several months, we looked at about a dozen houses. Some interesting stories to share.

One house had a great location, new condition, reasonable price. We were very satisfied. Then before leaving, the agent handed us a one-page report: “I must inform you — the wall in this house was previously found to have excessive methamphetamine levels. Here’s the test report.” I asked the agent what “methamphetamine” meant. He said, “It’s also called ‘P.’ Ever used P?” I thought — “P” is phosphorus on the periodic table — it’s in laundry detergent, even in the fried dough sticks made by unscrupulous Chinese vendors. Baby formula has phosphorus too. So I answered, “Yeah, I’ve used P. No big deal,” and happily left. Later I looked it up and nearly had a heart attack. The “P” wasn’t laundry detergent or baby formula — it was meth. “P” is New Zealand slang for crystal meth. Truly a decadent capitalist society where vice is everywhere. The people who lived there before must have been so high they contaminated the walls. The area had a severe drug problem — no way we’d buy there. Retreat.

Another house — we arrived a bit early before the Open Home. While wandering around, we met two curly-haired Māori girls who looked just like Moana. They enthusiastically chatted with us and showed us around — three bedrooms, two car parks — and kept saying, “You should buy this house!” I wondered if they were shills hired by the agent. “Why should we buy it?” I asked. They got excited: “If you buy it, you’ll have countless adorable bunnies! We came to see the bunnies!” They dragged us to the neighbour’s backyard, lifted a tarp, and — whoa — instant trypophobia trigger. Countless red rabbit eyes staring at us. New Zealand is truly a village — every house has plenty of space front and back. Chinese people like digging in the dirt and planting vegetable gardens. This Westerner was running a side business — rabbit farming to supplement his income. No wonder we’d smelled rabbit droppings as soon as we got out of the car. If we’d bought this house, we’d be smelling rabbit poop every day. No way. Retreat.

Another house was near where we used to live. We passed it every time we went to the park. It looked small and old, so it shouldn’t be expensive. We went to see it. The maintenance was terrible — moss-covered roof, walls peeling as if about to collapse. The asking price was NZ$1.6 million — luxury territory. I asked the agent what was up. He looked us up and down and said dismissively, “New here, huh? The house is small and run-down, but it sits on nearly 1,000 square metres of land. Developers call this a ‘big-land crappy house.’ This one’s a textbook example. The bigger the land and the crappier the house, the better — you can knock it down and build two or even three homes to flip. A crummy house is easier to demolish — ideally it collapses on its own so you don’t have to pay for demolition. You’re clearly not developers, so go cool your heels somewhere else.”

Another house had failed at auction. We went to check it out. It faced the street — noisy — but the interior was lavishly renovated. The agent’s asking price was way above its actual value. When asked about the owner, the agent said the house was empty. Curious — why renovate so luxuriously if nobody lives there? We asked about the previous sale record. The agent wouldn’t say. But NZ property records are public online. We checked: the house had been sold just over two years ago. Everything clicked. A textbook house-flipping case. The buyer followed the “7D principle” of the flipping guru: buy, renovate for good first impressions, then find a “bag holder.” The flipping guru has apprentices all over New Zealand, causing public outrage. Read this article for more: Flipping “Godfather” Angers New Zealanders: Asians Go Home!. But this guy clearly underestimated the efficiency of NZ renovation crews. In China, a migrant worker team can renovate a house in half a month. Here, workers haven’t been trained at Lanxiang — six months for a renovation is considered lightning speed. By the time the house was done, foreign exchange controls had kicked in, and bag holders were scarce. He might be stuck holding the bag himself.

We arrived late to one Open Home — the agent was about to leave, but we flagged him down at the intersection. He stuck his head out the car window: “Can you pay in full? Need a loan? If you need a loan, forget it.” I thought, what kind of seller is this demanding — no loans, full cash only? The house must be incredible! I was purely curious. I went to see it. Turns out, it wasn’t that the house was too good — quite the opposite. It was too terrible. So bad the bank deemed it worthless as collateral and refused to lend against it. The main issue was the material. Unlike most Chinese houses, which are concrete, NZ houses use whatever’s available locally — wood, stone, concrete, steel. During the 1980s and 1990s, the government’s quality oversight was extremely lax, resulting in a bunch of bizarre building materials. For example, this particular house — though it had four rooms and two floors — was made of plasterboard. Yes, the same stuff used to make tofu in China. Chinese call shoddy construction “tofu-dreg projects.” New Zealand went a step further — they used the raw material for tofu dregs as a building material. Who dares to argue? After decades, this house was practically falling apart. No wonder the bank refused to lend.

In the end, we shortlisted two houses: one owned by an Indian family, one by a Māori family. The Indian house had a smaller footprint but was in a livelier area — and miraculously, it didn’t smell of curry. The Māori house was a typical Kiwi home with large lawns front and back, but there was nothing for kilometres except residential houses. You had to drive everywhere. After choosing, we entered the thrilling auction stage. More on that next time.